This post is a high-level summary of the central ideas underlying the evaluation of the economic costs and benefits of addressing climate change. One of the primary goals here is to explore, at a fundamental level, what is actually meant by the terms “costs of climate change” and “costs of addressing climate change”. Another goal is to gently push back against overly-simplified narratives that frame climate change policy as either a lose-lose scenario (i.e., it harms the economy with no benefit to society) or an extreme win-win scenario (i.e., it stimulates the economy by creating green jobs while saving civilization from collapse). In other words, I want to be nuanced and consider the economic trade-offs that appear to be at play. Some upshots that are expounded upon in this post are:

- There are economic costs to climate change that increase with the magnitude of climate change.

- There are economic costs to addressing climate change (reducing greenhouse gas emissions).

- Both of the above costs tend to be measured in monetary values but they fundamentally represent forgone production of real goods and services.

- The forgone production comes about because goods and services are somehow being produced less efficiently (more input per unit output).

- The costs of climate change can be obvious (like the cost to rebuild infrastructure after a storm made worse by climate change) but even adaptation represents a cost of climate change because it implies the diversion of resources away from uses that would have produced alternative goods and services.

- Some pathways of addressing climate change, like improving energy efficiency, represents negative costs or direct economic benefits.

- Most pathways of addressing climate change do represent true costs, mostly because they require the diversion of resources away from the production of alternative goods and services.

- Under idealized circumstances, without externalities, free markets tend to settle on a price and quantity that maximizes economic wellbeing.

- Burning fossil fuels is not one of these idealized circumstances – greenhouse gas emissions represent a market failure (negative externality) because the costs of climate change are distributed across society (socialized) while the benefits of obtaining the energy are privatized.

- Market failures are not addressed by free market forces (by definition) and generally require government solutions.

- The optimal economic pathway for reducing greenhouse gas emissions can be calculated. Though quite uncertain, these calculations tend to show something broadly similar to the reductions committed to by most of the nations on Earth (according to their Intended Nationally Determined Contributions) under the Paris Agreement.

Introduction

Everything that humans materially value requires energy to produce and over the past several centuries, civilization has found that the burning of fossil fuels (coal, petroleum, and natural gas) has been one of the most effective means of obtaining this energy. Harnessing energy via fossil fuel combustion releases greenhouse gasses as a byproduct which go on to alter global biogeochemistry and climate.

Humanity has not yet come close to exhausting our natural reservoirs of fossil fuels. The combustion of all available fossil fuels would likely be sufficient to raise global temperatures by more than 18°F above pre-industrial levels (Winkelmann et al., 2015) which is a magnitude and rate of change only matched by catastrophic events like the End-Cretaceous impact that caused the extinction the dinosaurs as well as ~75% of all species on the planet. Among a myriad of other consequences (e.g., Field et al. 2014), this level of sustained global warming would probably entail an eventual 200 foot rise in sea level (about the height of a 20-story building)(Winkelmann et al., 2015) which would reshape much of the world’s coastlines and require a relocation of a large fraction of world population and infrastructure.

These negative consequences indicate that it would be optimal to reduce the emissions of greenhouse gasses over time. However, reducing greenhouse gas emissions comes at its own costs, especially if it is attempted to be done too quickly. In the most extreme case of halting all greenhouse gas emissions in a matter of days or weeks, global economic manufacturing and trade would need to be virtually shut down. The required restriction on the production and transportation of food alone would likely cause a global famine. Given the presumed undesirability of these two extreme cases (eventually combusting all available fossil fuels vs. halting all fossil fuel combustion instantaneously), humanity may be inclined to follow an intermediate path (e.g., Nordhaus, 1977).

Digression on fundamental market economics

We are all familiar with the idea that prices quantify how much something costs. So if we see that an electric car costs X thousands of dollars more than a gasoline-burning car, we have a sense that reducing greenhouse gas emissions by switching to an electric car has a net cost associated with it. Also, if we see that a weather disaster, made worse by climate change, costs X billions of dollars to recover from (e.g., Holmes, 2017), we have a sense that climate change can cause economic losses. Using dollar amounts to quantify costs is convenient but these price tags themselves can’t really explain the fundamentals behind the costs. In order to understand that, it is useful to think about the economy from first principles.

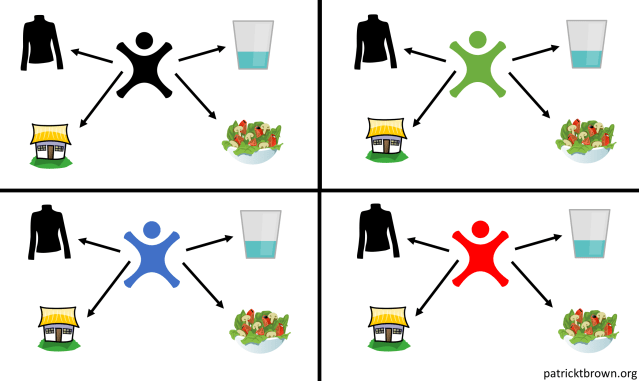

To start, let’s imagine a civilization with only four people who are isolated from each other. Due to their isolation, there is no trade between them and thus each of the four people is responsible for producing all of the things that they need to survive. So each person makes their own clothes, finds and decontaminates their own water, prepares their own food, and creates their own shelter. You can imagine that these tasks would take up almost all the time and energy of each of the individuals and there would be little time for leisure or to produce anything that would be considered to be a luxury. Thus, by modern standards, each of these four people would be living in extreme poverty.

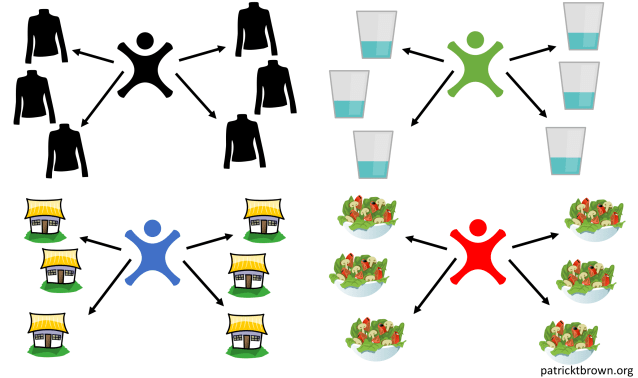

Now let’s imagine that the isolating barriers between these four people are lifted and they are allowed to trade with each other. This allows individuals to focus on producing the things that they are best at producing (or best at producing at the lowest opportunity cost) and trading for their other needs and desires. In this example, one person can focus on making clothes, one person can focus on producing drinking water, one person can focus on producing food and one person can focus on building shelter. Since each person does what they do best and since they can do these things better when they devote all of their time and effort to a given task, more of each product is produced.

In global macroeconomics, the total value of goods and services is measured in Gross World Product. In the case above, specialization has allowed the gross product of this hypothetical world to increase by 50%.

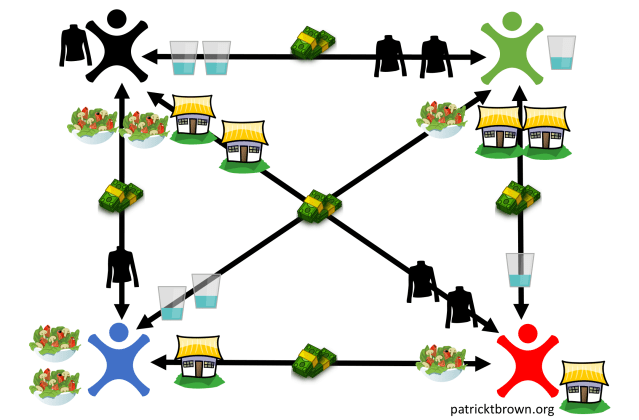

Specialization and trade thus make everybody better off than they would be if they were each responsible for only their own needs and desires. In practice, trade itself is made much more efficient by the use of money (rather than using a barter system) because this avoids the necessity of a double coincidence of wants.

It is important to note that money simply represents the medium of exchange and the store of value in an economy. The prices of each good are relative to other goods and relative to the total amount of money in the economy. The wealth of the world is not measured by how much money there is. If we triple the amount of money in this world, nobody becomes better off (i.e., there are no new goods produced and real Gross World Product does not increase). All that happens is that the prices of everything go up by a factor of 3 (you get monetary inflation).

When economist cite numbers for Gross World Product (or Gross Domestic Product) they usually correct for any monetary inflation. Thus, Gross World Product is expressed in some standardized monetary value but it refers to actual goods and services. You can increase real Gross World Product by increasing the real amount of goods and services in the economy (e.g., through increased efficiency of production through increased specialization and trade) but you can’t increase real Gross World Product by simply increasing the amount of money in the economy.

It is also interesting to note that in our hypothetical world with specialization and trade, everyone still has basic subsistence needs and these needs are still being met by people working most of the day. Each person, however, is insulated from the production of some of the items that satisfy their own basic needs because they are trading for them rather than directly producing them. When someone uses the expression that they need to go work in an office all day in order to “put food on the table” they are not simply making an observation about their proximate motivations to go to work. Instead, they are making a fundamental observation about how specialization and trade literally underpins one’s ability to survive. Unfortunately, we do not live in a paradise Garden of Eden where all our needs and desires are magically satisfied without the exertion of human effort. In the idealized situation described here, individuals can either produce for their own needs and desires or they can produce something else that they can trade in exchange for products that satisfy their needs and desires1. This is essentially what all working people are doing in modern market economies.

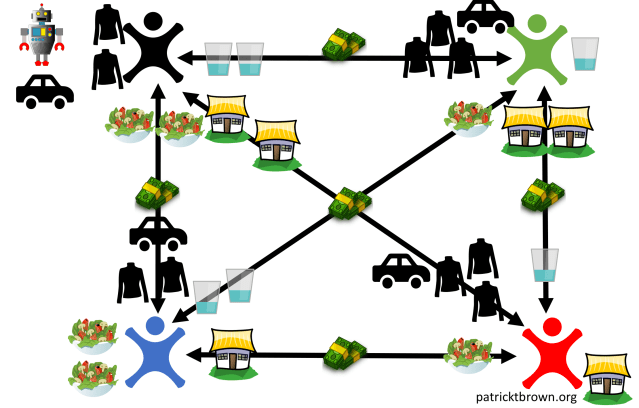

Now let’s imagine that one of the people in our hypothetical world, the clothes maker, invents a clothes-making robot. This has two main effects: It allows for more clothes to be produced per unit time and it liberates some of the time of the clothes maker. The clothes maker can then use their extra time for more leisure or they can choose to use some of their extra time to produce something other than clothes. Let’s say they use their extra time to invent a mode of transportation which they themselves use and can also trade to others.

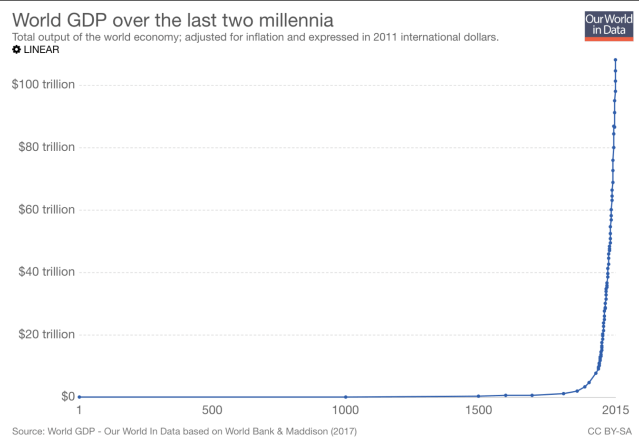

Now everyone in the society has more clothes and everyone also has a mode of transportation. The Gross World Product has grown. Specifically, the Gross World Product has grown because automation (the robot) took a job (making clothes) which liberated the time and energy of the former clothes maker and allowed them to put effort into another project2. This is one of the primary processes responsible for the explosion in global economic production of the past few centuries:

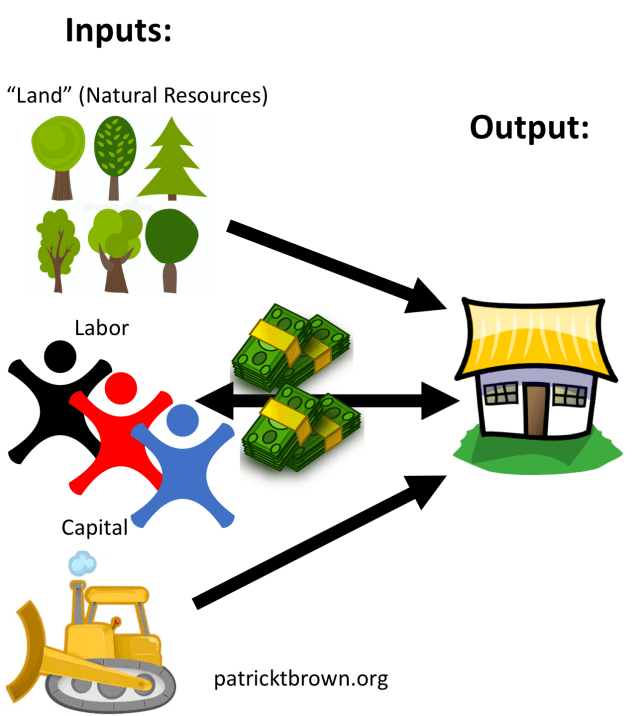

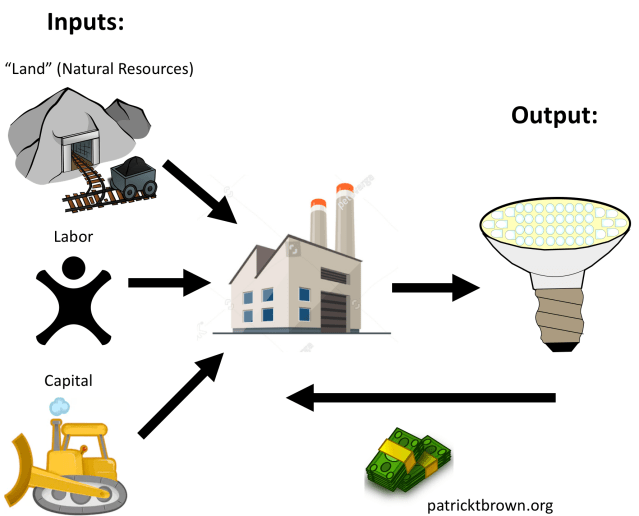

This digression using an ultra-simplified hypothetical world, serves to make the point that when we are talking about economic well-being, we are not simply talking about price tags and wages. Instead, economic well-being has more to do with the efficiency by which societies are able to convert various raw inputs into goods and services (Gross World Product). These inputs are often called the factors of production and are sometimes divided into the categories of land (natural resources), labor (hours worked by people) and physical capital (technology used to make products). These inputs come together to produce output like, e.g., shelter.

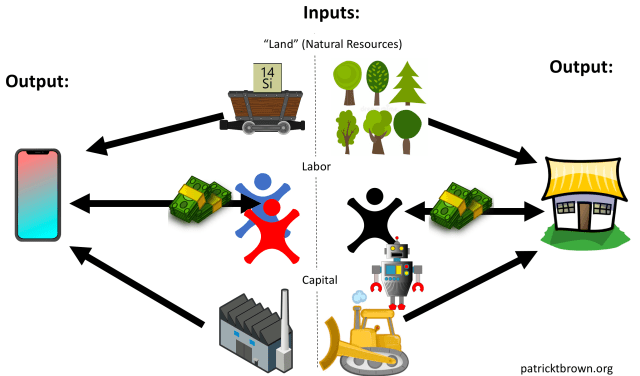

Now let’s imagine that the labor necessary for producing shelter gets reduced because of some improvements in technology (e.g., an improvement in technology allows some of the tasks to get automated). This means that it now takes less input (labor has been reduced) to produce the same output. Since it takes less input, the cost of the output has decreased. In this case, it makes the buyers of shelter (everyone) better off since they can now get shelter at a lower price (i.e., for trading less of the goods and services that they produce). This also has the effect of liberating labor to do other things like produce, say new communication technology3.

The costs of climate change and the costs of addressing climate change

The upshot of the above digression is that from a zoomed-out, macroeconomic perspective, a change that allows for production to become more efficient (in terms of inputs per unit output) causes more Gross World Product to be produced and thus is considered to be a net economic benefit. On the other hand, if some change makes production less efficient (in terms of input per unit output) then there is a net cost to Gross World Product and the economy. There are costs associated with climate change (sometimes called damages) and there are costs associated with addressing climate change. Let’s look at how these come about.

The costs of climate change

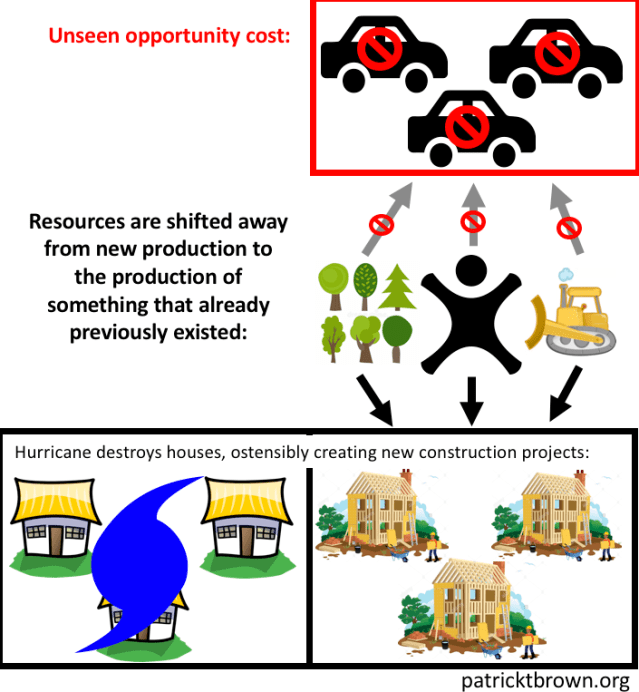

It is perhaps not surprising that the direct destruction of infrastructure from natural disasters constitutes economic losses. For example, climate change is expected to increase the intensity of the most intense hurricanes. Obviously, the destruction of lives and livelihoods that result from more intense hurricanes is a bad thing but some people might be tempted to imagine that there is a silver lining to this destruction. Won’t this destruction have some stimulating effect on the economy? Won’t this destruction create jobs in construction companies and in manufacturing? Won’t this all stimulate economic growth? It may be the case that a particular underemployed individual or community might benefit from these new construction projects but from a zoomed-out macroeconomic perspective, these projects represent a cost on the economy. This is because, when these destroyed homes are rebuilt, they are rebuilt at an opportunity cost: inputs that would have been used for producing something else are used instead to rebuild houses that already previously existed. Thus, rebuilding these homes does not stimulate the overall economy by, e.g., producing jobs. If this were the case, we could stimulate the economy by simply bulldozing homes every day and having people rebuild them.

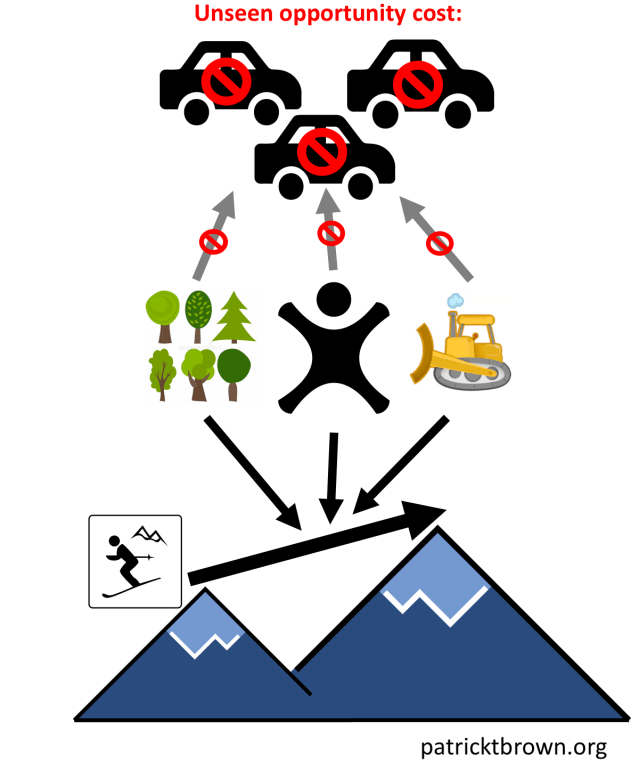

Climate change can also impose economic costs through pathways that are disguised as “adaptation”. Fundamentally, these costs come about because human society, as well as our natural resources, are adapted to the current climate. So even if things change, but they aren’t changing in an obviously negative direction, it is still a cost to adapt to those changes.

To take a seemly benign example, imagine that as the world warms, ski resorts must be moved from lower elevations to higher elevations and from lower latitudes to higher latitudes in order to follow the snow. Again, this change may seem as though it is economically stimulating. After all, construction of these new ski resorts will appear to create jobs. But again, from a zoomed-out macroeconomic perspective, this adaptation represents a net cost to society. The reason is that construction of the new ski resorts require inputs and the net result is not new output but rather a replacement ski resort that only gets society back to where it started (in this case, one ski resort). Furthermore, the inputs required to create the new ski resort are used at an opportunity cost: something else that would have been created with them (like say, modes of transportation) are forgone. The overall result is that there is a net loss of Gross World Product due to the adaptation.

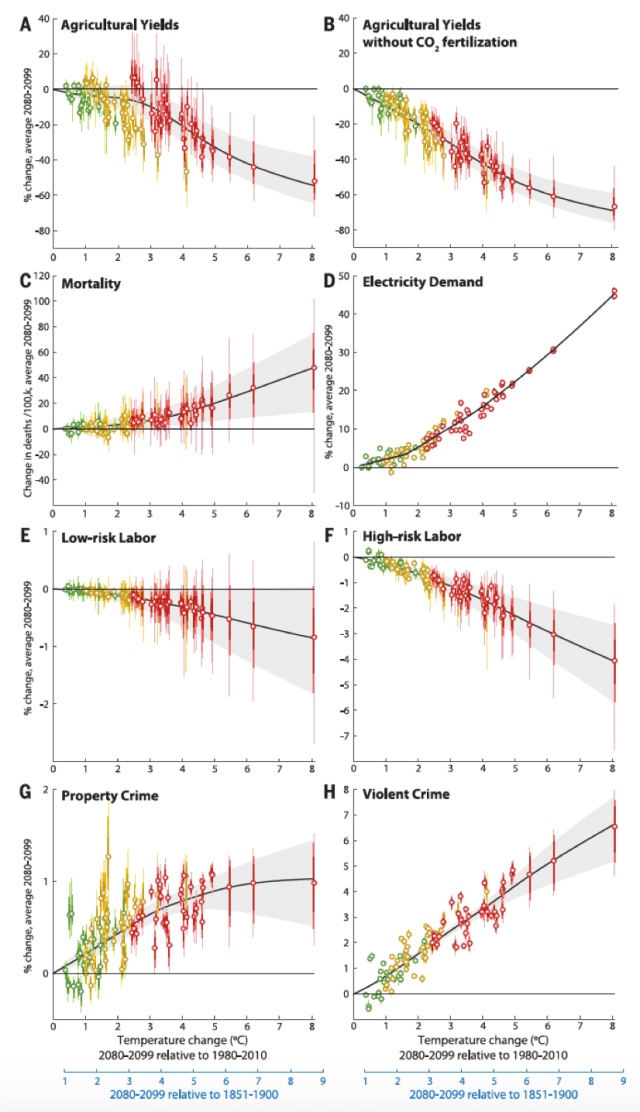

Some of the real-world pathways by which climate change is supposed to harm the economy are through changes in agricultural yields, sea level rise, damage from extreme events, energy demand, labor efficiency, human health and even human conflict. These phenomena are diverse but in all these cases, the true economic cost comes about because less output (goods and services) ends up being produced per unit input.

From Hsiang et al. (2017)

The costs of addressing climate change

In order to address climate change, we need to find ways of harnessing energy without emitting greenhouse gasses. In some circumstances, this can be done at negative costs or with economic benefits. For example, increases in energy efficiency of some services, such as lighting, constitutes less input per unit output. Thus increasing energy efficiency (and holding everything else constant) would provide an economic benefit and reduce climate change at the same time.

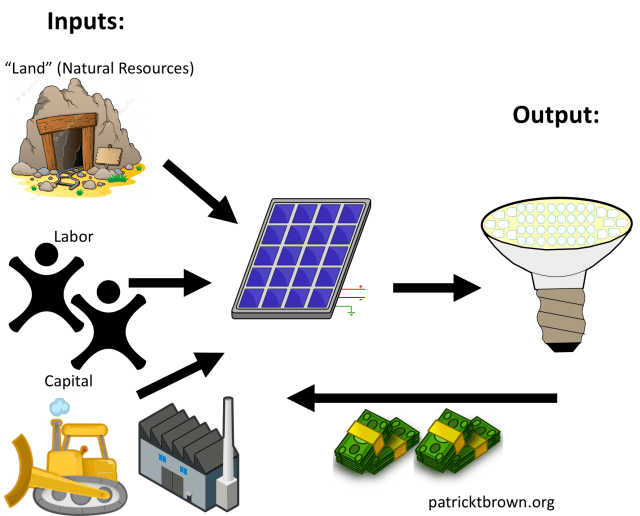

Unfortunately, most of the actions associated with addressing climate change do come at an economic cost. These are typically called abatement costs or mitigation costs. Fossil fuels represent the accumulation of solar energy over millions of years that we can release simply by digging it up and burning it. Non-fossil fuel (i.e., “alternative” or “renewable”) sources of energy tend to be more expensive partly because the energy source is more diffuse or more variable and thus produces less output (Joules of useable energy) per unit input.

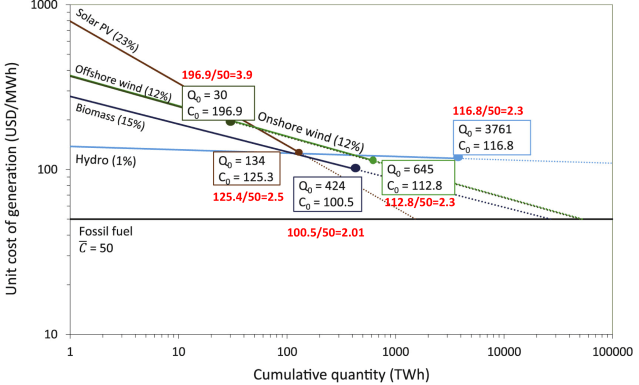

Renewable energy is coming down in cost steadily as technology advances and it is already cheaper than traditional sources of energy in many specific circumstances. However, there is still a long way to go before renewable energy is at cost-parity with fossil fuel combustion in terms of being able to provide all the energy necessary to power society. This is reflected in the current price ratios of renewable energy relative to fossil fuel energy shown in red:

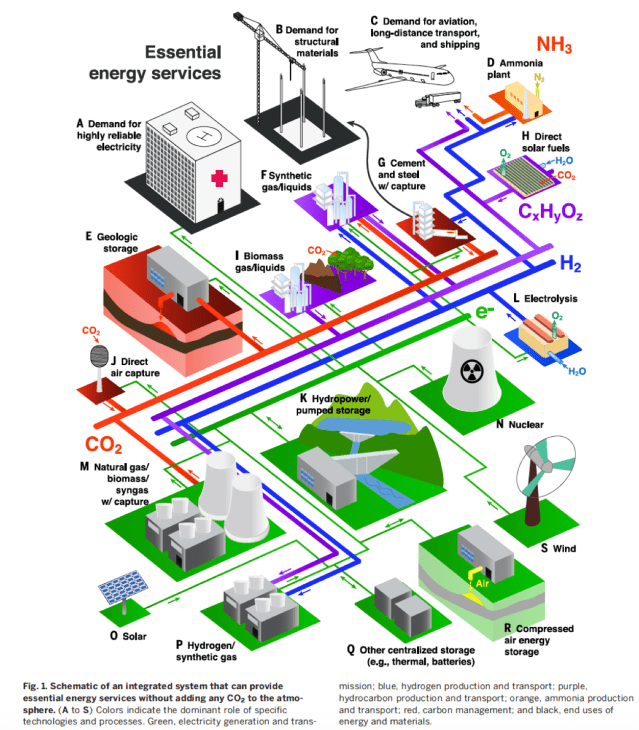

We can readily imagine a technically-feasible future energy infrastructure that eliminates greenhouse gas emissions:

From Davis et al. (2018)

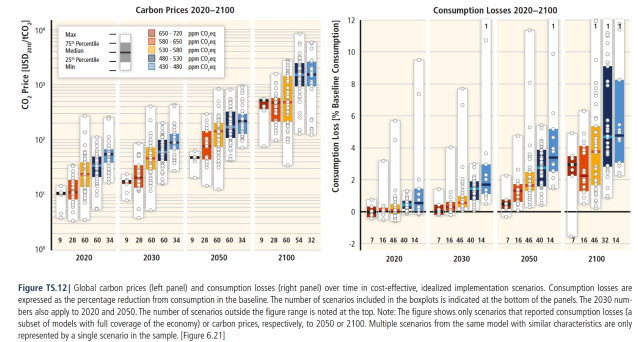

However, achieving the above transformation comes at a cost. This is because, over the past two centuries, the global energy-producing infrastructure, along with the associated human institutions and behaviors, have matured in coordination with technologies that burn fossil fuels that emit greenhouse gasses as a byproduct. As of this writing, ~80% of the 18 terawatts necessary to power global civilization still originates from these fossil-fuel burning systems. Thus, reorganizing this infrastructure will require a great deal of resources to be reallocated from alternative uses in order to get roughly the same amount of energy that could have been produced from burning fossil fuels. This comes at an opportunity cost of forgone production in other areas and thus constitutes a cost on global economic production. The net costs on the global economy have been estimated to be between ~2% and ~10% of consumption (which is Gross World Product minus investment) by 2100 for the proposals that would limit warming to the greatest degree:

Addressing climate change through government regulation

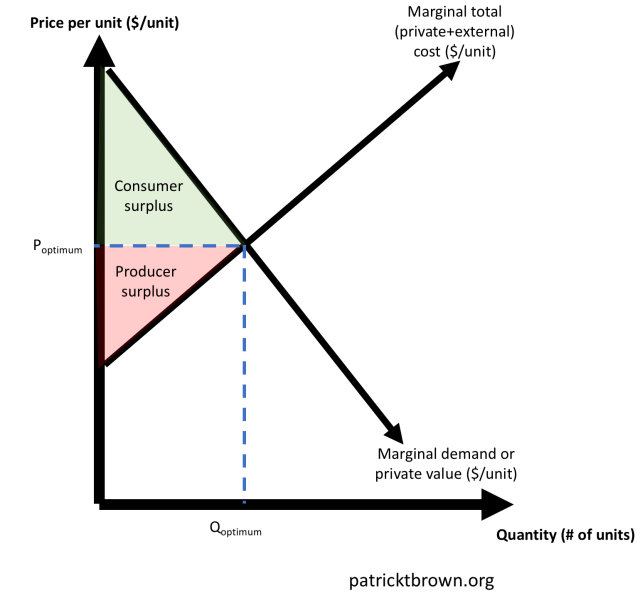

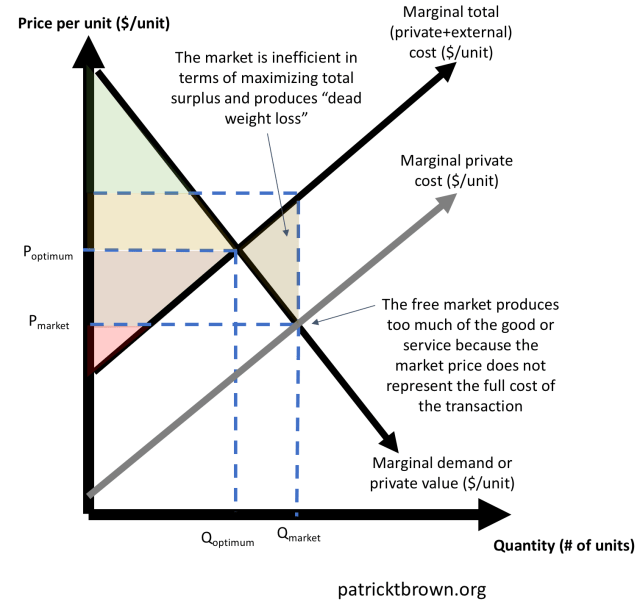

The aforementioned costs associated with climate change itself (damages) are what justify governmental policies designed to limit climate change. This is probably best understood in the framework of total surplus from welfare economics. In this framework, the total economic well-being of society can be measured in terms of consumer surplus plus producer surplus. Consumer surplus is the difference between what a person is willing to pay for a good or service and that they actually pay. So if I am willing to pay $700 for a refrigerator and I buy one for $500, then I have a consumer surplus of $200 and feel as though I have gotten a good deal. Producer surplus is the difference between what it costs to produce a good or service and what that good or service is sold for. So if it costs $200 to produce the aforementioned refrigerator, then the producer surplus in our transaction was also $200 and the total surplus was $200+$200=$400. This is represented graphically with marginal supply and demand curves like those below.

The demand curve illustrates that as the price goes up, there will be less demand and the supply curve illustrates that as the price goes up there will be more supply. Trade will occur as long as the producer receives producer surplus and the consumer receives consumer surplus. In a competitive free market with perfect information, the price will equilibrate at the point that maximizes total surplus (consumer plus producer surplus) and thus maximizes the total economic well-being of society. This was proven under certain assumptions in the fundamental theorem of welfare economics.

A problem occurs, however, when the costs of the transaction are not fully born by the producer. This is called a negative externality. Pollution (like human-caused CO2 emissions) is the quintessential negative externality. In a situation with a negative externality, a free market will naturally produce a price for a product that is too low and thus too much of the product will be produced. The external cost to society from CO2 emissions is quantified by the economic damages associated with climate change (and is formally quantified in policy circles with the Social Cost of Carbon). Under this situation, the free market has failed to produce the economically efficient outcome and thus it is justifiable (if the goal is to maximize total surplus) for the government to step in and raise the price of production (through e.g., a tax) to a price that would maximize total surplus4. This is called a Pigovian tax and is one of the main policy pathways by which climate change can be addressed5.

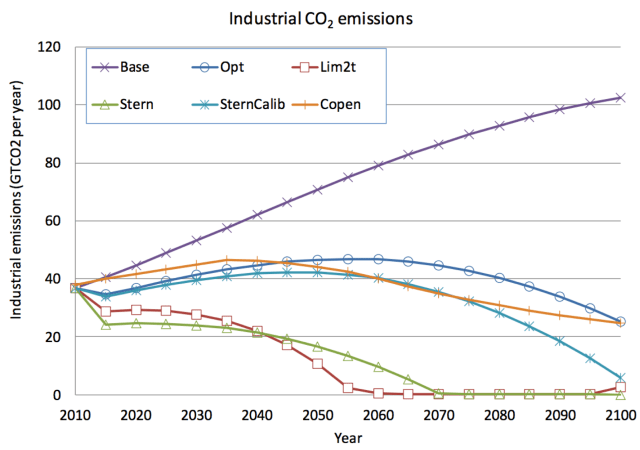

So there is an economic cost to climate change, there is a cost to addressing climate change and there is a mechanism (a government tax) that can correct the market failure and divert resources away from activities that emit greenhouse gasses. Can these three ingredients be taken into consideration simultaneously in order to evaluate the best pathway for society going forward? Yes, they can. This task has typically been undertaken with Integrated Assessment Models (IAMs). The three highest-profile of these models (and the three models used by the U.S. government to estimate the global Social Cost of Carbon) are FUND, PAGE and DICE. These models weigh the benefits of avoided economic damages from climate change against the costs of mitigating greenhouse gas emissions and calculate the optimal carbon tax and global greenhouse gas emissions reduction pathway such that the net present value of global social welfare is maximized (see “Opt” pathway below).

From Nordhaus (2013)

The “Opt” pathway above results in global temperatures stabilizing at levels roughly near 3 degrees Celsius which is comparable to what would probably result from countries’ currently agreed-upon Intended Nationally Determined Contributions under the Paris Agreement6.

Conclusion

Fundamentally, economics is all about real goods and services and the efficiency by which they are produced. Economic costs are incurred when something changes such that it becomes less efficient to produce goods and services (less output per unit input). Both climate change itself (the problem) and addressing climate change (the solution) present economic costs because they require resources to be reallocated away from alternative uses in such a way that total production is less efficient. One strategy of dealing with climate change is to correct for market failures by increasing the cost of greenhouse gas emissions to their true total cost. The time dimension (and cost of alternative energy) can be taken into consideration by using Integrated Assessment Models. These models tend to calculate that the optimal economic pathway entails a reduction in greenhouse gas emissions through the remainder of the 21st century in a pathway somewhat similar to what countries have agreed upon under the Paris Agreement.

Footnotes

- Of course, most societies have decided that it is undesirable to allow people to completely fail in a competitive market and thus starve to death. This is particularly the case when some misfortune has made it so that a given person is not able to trade a valuable good or service. Thus, social safety nets have been implemented which essentially mandate that some portion of society subsidize another portion of society without compensation.

- Notice that the person who invented the clothes-making-robot is now producing more than some of the other people in the society. The other people are indicating that they value the clothes and transportation more than some of the money that they have and thus they are sending money to the clothes maker in voluntary win-win transactions. Thus, the clothes-maker will accumulate money in proportion to the real wealth that they have created for society. In other words, they are not becoming rich at the expense of other members of the society but instead, their monetary wealth is an indication that they have created real wealth that is valued by the rest of society. Thus, in an idealized market-based economy like the one being described here, monetary wealth will end up being distributed to individuals in proportion to the real physical wealth that they produce. Monetary wealth will not necessarily be distributed in proportion to how much/hard people work or how “moral”/“good” their work might be, as judged by a 3rd party.

- Although simplified, this is analogous to what has been going on in the real world. For example, in 1820, approximately 72% of the American workforce were farmers. Advances in technology have allowed much more food to be produced with less labor and thus US GDP has exploded over the same time period that those farm jobs were eliminated.

- Incidentally, the justification for government funding (subsidizing) science is the reverse of this situation. Specifically, it is the recognition that scientific discoveries represent a positive externality. Under a positive (consumer) externality, the total demand (private+external) is larger than the private demand alone and thus the free market produces too few scientific discoveries at too low a price.

- To the extent that fossil fuels are subsidized rather than taxed, this further distorts the market away from its optimal price and quantity. Removing these subsidies would also constitute negative mitigation costs.

- Of course, the Paris Agreement’s goal was not to optimize for Gross World Product. The most stringent targets can be thought of as being more optimal in terms of Natural Capital or “non-market” goods that have less tangible value than commodities that are regularly bought and sold in markets.

Patrick –

There’s a lot to this post, and so a lot to look over. I just wanted to drop off a few quick comments:

You say:

> “The external cost to society from CO2 emissions is quantified by the economic damages associated with climate change (and is formally quantified in policy circles with the Social Cost of Carbon).

My own view is that a more expansive view of externalities is relevant. There are significant externalities associated with fossil fuel usage – even if not that all of them directly associated with CO2 emissions – which I think are an important part of the picture. For example, there are the external costs associated with black carbon emissions. There are external costs associated with the geo-political realities of keeping oil flowing (e.g., fighting expensive wars for, at least to some extent, keeping access to fossil fuels; empowering autocratic governments that limit the rights and human capital for large percentages of their populations – at huge economic costs from a counterfactual angle). And, even perhaps more indirectly there are negative externalities such as the costs of building roads or costs of urban sprawl or loss of from productivity from traffic jams, in the form of opportunity cost that stems from a reliance on combustion engine, individual user transportation powered by fossil fuels and largely a result of the powerful influence of the fossil fuels industries. IOW, consider the “costs” not building out, instead, mass public transportation, perhaps even mass public transportation powered by renewable energy.

That isn’t to say that positive externalities aren’t also relevant. But one problem, IMO, is that people tend to bake indrect positive externalities into the cake – taking them for granted in that fossil fuels support economic growth – w/o really working hard to quantify the positive/negative ratio of those indirect externalities. That is a hugely difficult task, no doubt. Trying to assess the indirect opportunity cost of relying on gasoline to power automobiles and not moving towards greater use of public transportation, is enormously complicated. As such, I can understand where people are naturally resistant to take on that task to assess the costs and benefits to fossil fuel usage; but I think it is an important task, and that it is particularly important to take a balanced approach; it is important to not take those indirect positive externalities for granted while effectively ignoring the indirect negative externalities.

You also say:

>Most pathways of addressing climate change do represent true costs, mostly because they require the diversion of resources away from the production of alternative goods and services.

This, IMO, seems to assume, broadly speaking, a conclusion with respect to the positive/negative external cost ratio of using fossil fuels as compared to alternative energy sources. In other words, assessing the cost of diversion of resources away from alternative goods and services is far from straight-forward, IMO.